A diversified supply base proves key to reliable service as freight market surges

Over the past 2 months, imbalances in the freight market began leveling out. Much of the US started reopening, and shippers across the country began harvesting their goods for produce season. Trends across volume, rates, and facility ratings signaled a strong recovery after months of turbulence.

As freight volumes picked up, shippers leaned on APIs to save time and resources. Carriers showed a preference for the spot market, which, according to the DHL Supply Chain Pricing Power Index, resulted in an increase in tender rejections throughout June. Some shippers were negatively affected, while those that invested early in broad, diversified carrier bases maintained reliable service despite tight capacity.

Growing volume and higher rates see carriers turn to the spot market

As states across the country loosened restrictions and started preparing for summer, the freight market tightened and, building on the gains made in May, began to swing in carriers’ favor. Volumes spiked across the country, as much as 15% month over month in the West and 10% in the Southeast, driving up rates and bringing much-needed relief to carriers coming out of the dry spell of March and April. Van and reefer volumes in particular rose 23% and 7%, respectively (according to FreightWaves).

With volume increases came another surge in spot loads, and carriers seized the opportunity. Spot volume overall grew 44% from May to June, and rates followed suit. Van and reefer spot rates jumped 21% and 12%, respectively, month over month.

Shippers react to tight market conditions by leveraging pricing APIs

As volumes surged and spot market volume increased, shippers began moving toward APIs in droves in order to manage the influx of demand efficiently. Overall API volumes with Uber Freight grew from May to June by 15%.

This trend held especially true in regions that loosened COVID restrictions earlier on; the Southeast saw a 23% increase and the Midwest saw a 13% jump. Produce import and export also played a role as we entered the produce season’s peak; the West, a key region for stone fruits, avocados, and potatoes, saw a 49% increase in API volume over the same time period.

The connection between tight markets and an uptick in API loads was most apparent in California, Texas, and Georgia. All 3 markets experienced the highest increases in volume and number of API loads, demonstrating the ability of APIs to provide superior and timely service to shippers in a bind.

Continued API growth shows that shippers are increasingly depending on the flexibility and transparency that digital tools offer to navigate unpredictable market fluctuations.

Tender acceptance is higher where the supply mix is diversified

With a tight market and surging spot volumes, some shippers started to see an increase in contract freight being rejected. According to FreightWaves, overall tender rejections were up nearly 10% week over week for the first half of June. Shippers with diversified supply bases, either their own managed supply or through marketplace partners like Uber Freight, were able to navigate a fickle carrier market and maintain higher rates of tender acceptance by relying on multiple carriers to move loads. Part of the value of partnering with Uber Freight is having access to a liquid marketplace of nearly 60,000 carriers, meaning reliability of service is consistently high.

Throughout market fluctuations, Uber Freight’s core focus was to maintain tender acceptance rates, meet or exceed customer expectations, and keep freight moving. As a result, throughout May and June, Uber Freight maintained national tender acceptance rates above customer set thresholds demonstrating reliability where secondary routing guides wavered.

| June low | June high | |

| Midwest | 92.46% | 97.72% |

| Northeast | 93.93% | 99.49% |

| Southeast | 90.04% | 99.14% |

| Southwest | 90.81% | 99.19% |

| West | 95.63% | 99.00% |

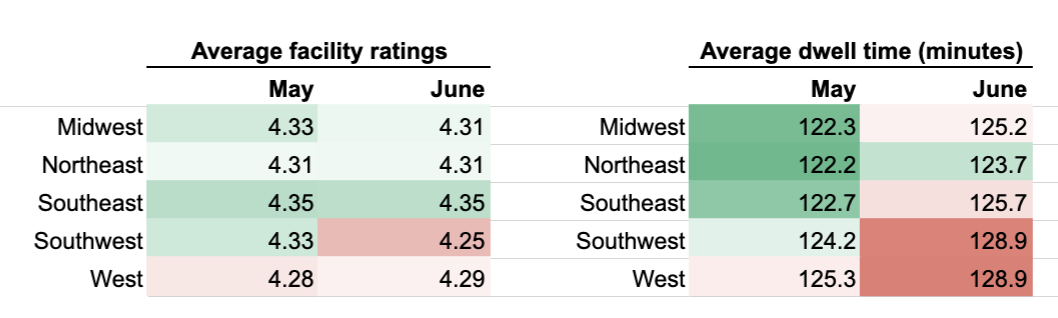

Facility ratings stabilize despite increases

Increased volumes across the country caused a slight increase in dwell times, particularly in the West and Southwest, which saw 3.7% and 2.9% increases, respectively. The Southwest saw a slight drop in facility ratings, potentially as a result, but the majority of facility ratings held steady across the country.

This is the third in a series dedicated to understanding supply chain pressures caused by COVID-19, drawn from trends Uber Freight is observing across our own marketplace. Learn more about optimizing shipper operations with APIs from Uber in the latest blog post from our Head of Operations, Bill Driegert.

Uber Freight