Unpredictable consumer behavior leads to a tight market in July

In May and June, the freight market leveled out, with produce season in full swing and consumer behavior kicking back up. The latest data and research from Uber Freight shows an unseasonably tight market in July with volumes continuing to trend upward.

While shippers work to keep up with erratic consumer demands and lingering impacts from COVID-19 lockdowns, carriers are seeing higher facility wait times but higher rates, helping to make up revenue lost in the early days of the pandemic.

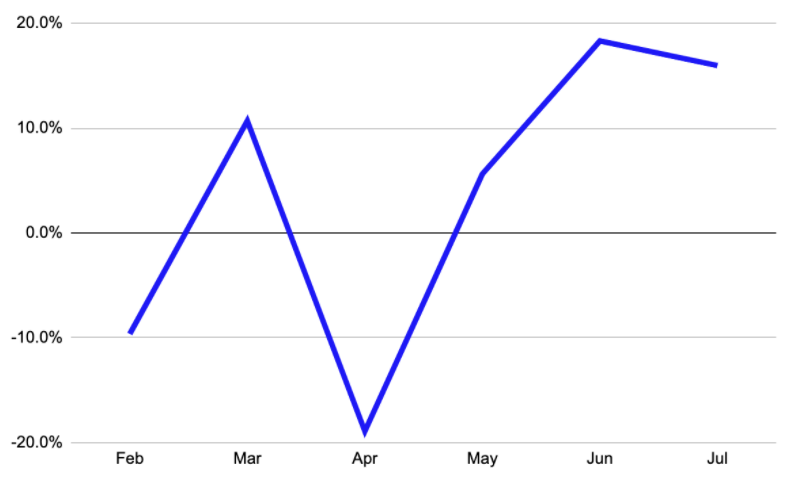

The market is uncharacteristically tight as rates continue rising

July saw substantial, double-digit rate increases across regions and modalities. Van rates increased by an average of 15% from June to July, compared with -5% in the same time last year. In the Southwest, van rates were up 18%. Nationwide reefer rates, the most volatile throughout the pandemic, began to tick up in May and have continued to rise—increasing 14% since June.

Normally, the market loosens up after a Fourth of July surge, specifically as beverage demand from the summer tapers off. This year, though, there are uncharacteristically high volumes in food and beverage as people forgo restaurant visits for grocery stock-ups. This is resulting in a tight market as shippers work to meet extended consumer demand.

Carriers take advantage of a market in their favor

With the market deviating from expected seasonal trends, shippers are grappling with disrupted supply chains. Despite higher costs, shippers are tendering more spot loads to guarantee capacity at a time when rejection rates are high. In return, carriers are taking advantage of the lucrative spot market, with a 31% jump in rates from June to July. This increased dependence on spot freight signals a reluctance to enter into long-term contracts for fear of future market fluctuations and unpredictable consumer demand.

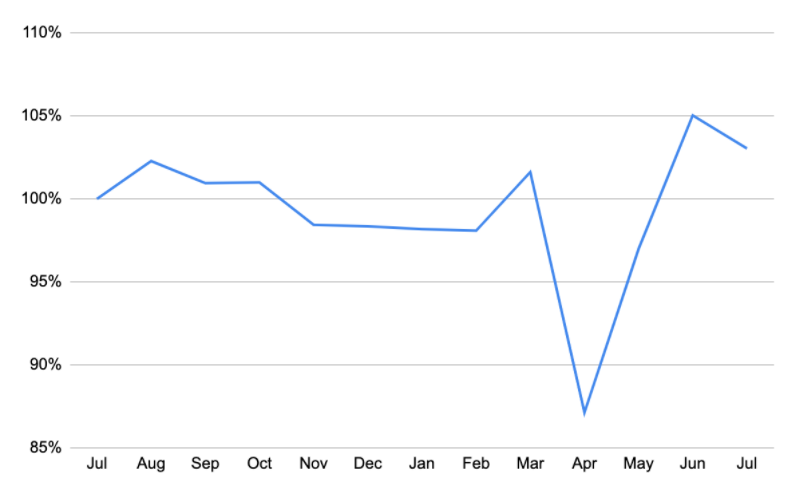

In April, drivers were driving fewer miles daily—approximately 14% fewer—as low rates and an uncertain market kept them either close to home or not driving at all. In May, mileage bounced back to normal. In June, it then jumped up to the highest levels seen in over a year, remaining slightly elevated in July.

Dwell times rise as facilities grapple with volume increases

After plummeting in March and April, facility ratings in May and June began to resemble pre-COVID levels. In July, though, as supply chains were tested by higher volumes and market imbalances, facility efficiencies began to lag again. In all regions except the Southwest, ratings fell, and dwell times rose an average of 3.3 minutes from June to July, which is the highest they’ve been nationwide since the pandemic began. The West had the highest dwell times out of any region for the third month in a row.

This is the fourth in a series dedicated to understanding supply chain pressures caused by the COVID-19 pandemic, drawn from trends Uber Freight is observing across our own marketplace.

Uber Freight